Complying with the CSRD directive but not sure where to start? In this blog, we provide a complete overview of what the CSRD entails, which companies need to comply, what must be reported, and what the key deadlines are. Whether you are already familiar with the predecessor of the directive (NFRD) or dealing with sustainability reporting for the first time – this blog offers you all the information in one place.

The CSRD (Corporate Sustainability Reporting Directive) is a European directive that requires companies to report more extensively on their environmental, social, and governance (ESG) impacts. This means companies must explain how they address topics like climate change, human rights, and sustainable business management.

The goal of the CSRD is to improve transparency, allowing investors, customers, and other stakeholders to better understand a company’s sustainability. Additionally, companies must indicate whether issues like climate change could affect the company’s financial value.

Under the Corporate Sustainability Reporting Directive (CSRD), companies are required to report on a broad range of sustainability-related topics. These fall under the categories of Environmental, Social, and Governance (ESG). Below, we outline what is specifically included under these categories.

Environment

The E in the ESG categories stands for Environmental. This includes three subcategories that must be reported on:

- Climate change. This includes, among other things, CO2 emissions, energy consumption, and the use of renewable energy within your organization.

- Water and waste management. This concerns water usage, water pollution, and waste processing methods within your organization.

- Biodiversity. Here, you must report on aspects such as the impact of your business activities on ecosystems and biodiversity.

Social

The S in the ESG categories stands for Social. This includes three subcategories that must be reported on.

- Working conditions. This includes aspects such as the level of diversity and inclusion, workplace safety, and labor rights.

- Human rights. This pertains to compliance with international standards and any human rights violations within your organization’s value chain.

- Relationships with stakeholders. This focuses on how your company engages with employees, customers, and communities.

Governance

The G in the ESG categories stands for Governance. This includes two subcategories that must be reported on.

- Business ethics. This includes anti-corruption measures and regulatory compliance within your organization.

- Governance structure. This focuses on the composition of the board, responsibilities, and compensation policies within your organization.

The time required to report under the CSRD depends on the size of the company, the complexity of its activities, and whether the company already has experience with sustainability reporting.

The primary time investment involves gathering data on ESG aspects such as CO2 emissions, energy consumption, and employee rights. Once this data is collected, it needs to be analyzed and integrated into the sustainability report. Since the CSRD affects various parts of the organization, collaboration is required across departments such as finance, operations, and HR.

Additionally, an external audit of the reports is mandatory, which can add time and resources, depending on the scope of the reporting. Overall, the initial CSRD reporting process may take several months to prepare and implement. In subsequent years, the time investment may decrease as processes become more streamlined

The CSRD applies to a wide range of companies within the European Union. The requirement depends on the type and size of the organization. Below, we provide a detailed overview.

Large companies that fall under the Non-Financial Reporting Directive (NFRD)

These companies are already required by the NFRD to prepare non-financial reports. This includes companies with more than 250 employees, a turnover exceeding 40 million euros, or a balance sheet total of more than 20 million euros.

Large companies that do not fall under the NFRD

This group of large companies is not covered by the NFRD but will soon be subject to reporting obligations under the expanded CSRD regulations. This also includes companies with more than 250 employees, a turnover exceeding 40 million euros, or a balance sheet total of more than 20 million euros.

Medium-sized listed companies

Medium-sized listed companies are also subject to the CSRD reporting requirements. This applies to companies with fewer than 250 employees but that are publicly listed within the EU. Despite their smaller size, their stock market listing requires them to comply with the stricter CSRD standards.

Small and medium-sized listed companies (SMEs)

Listed SMEs, with fewer than 250 employees, also fall under the CSRD. However, these companies are granted a transition period until 2026 to prepare for the new reporting obligations. More details on deadlines will follow later.

Non-European companies with activities in the EU

Companies based outside the EU that generate more than 150 million euros in revenue within the EU and have at least one subsidiary or branch in the EU are also subject to the CSRD. These companies must report on their sustainability impact within the EU, even though they are not directly under European regulations.

Large financial institutions

This includes banks, insurers, and other financial institutions that are regulated under EU legislation. Regardless of whether they meet revenue and employee criteria, they are required to report under the CSRD due to their role in the European financial system and the impact they can have on sustainability.

Under the new CSRD regulations, the deadlines for submitting sustainability reports vary by type of organization. The exact date for reporting depends on factors such as company size, whether the company is publicly listed, and whether it operates within or outside the EU. Below is an overview of reporting years and submission deadlines.

Large companies that fall under the Non-Financial Reporting Directive (NFRD)

- Translation: Deadline for delivery: 2025, for the fiscal year 2024.

- First reporting year: Fiscal year 2024

Large companies that do not fall under the NFRD.

- First reporting year: Fiscal year 2024

- Deadline for delivery: 2025, for the fiscal year 2024.

Medium-sized publicly traded companies.

- First reporting year: Fiscal year 2024

- Deadline for delivery: 2025, for the fiscal year 2024.

Small and medium-sized publicly traded companies (SMEs).

- First reporting year: Fiscal year 2025

- Deadline for delivery: 2026, for the fiscal year 2025

- Extension option: These companies can choose to report only in 2028, with an exemption for the fiscal years 2026 and 2027.

Non-European companies with activities in the EU.

- First reporting year: Fiscal year 2026

- Deadline for delivery: 2028, for the fiscal year 2026.

Companies in this category that need more time to get their systems and processes in order are not required to submit their first report for the fiscal year 2026 until 2028 at the latest.

Large financial institutions.

- First reporting year: Fiscal year 2024

- Deadline for delivery: 2025, for the fiscal year 2024.

Good to know: The exact deadline for delivering sustainability reports under the CSRD coincides with the publication of the annual report, which typically must occur within six months after the end of the fiscal year. For many companies with a fiscal year running from January to December, this means that sustainability reports must be submitted by June 2025 at the latest for the fiscal year.

The implementation of the CSRD brings obligations for companies in the EU regarding the content of the reports as well as the deadlines. Although some companies do not need to submit their first report until 2025 or later, it is wise to start preparing this year. This involves setting up systems, training staff, and collecting data to meet the requirements of the CSRD. This way, you won’t be under stress later on.

The reporting obligation of the CSRD is not something that can be done in a couple of moments. It's understandable that you want to know what steps the reporting entails. Below, we will go through it step by step.

Step 1. The materiality analysis

To determine which sustainability factors (ESG: Environmental, Social, and Governance) are relevant for your organization, a materiality analysis is an important first step. This analysis closely aligns with the requirements of the CSRD, including the concept of double materiality. This means that it looks at both the company's impact on the environment and society, as well as the impact on the company's own sustainability efforts.

Step 2. Integrate sustainability into business strategy.

The CSRD requires companies not only to report but also to demonstrate how sustainability is integrated into their business strategy. To meet this requirement, it is important to develop a clear plan for sustainability, with objectives that align with your company's long-term strategy.

Step 3. The first report

Reporting can begin. Document the required data for the fiscal year your organization needs to report on. It is important that your reporting complies with the ESRS standards for reporting formats and content. This includes: double materiality, ESG categories, quantitative and qualitative reporting (both figures and policies and objectives), assurance and audits (verification by an external party), and public accessibility.

Step 4. Assurance and control

The CSRD requires that the sustainability data be verified by an external party. This can be an auditor or another entity.

Step 5. Submitting the report

The time has come. You can submit the report to the relevant authorities. As mentioned earlier, the deadlines for submitting reports vary (you can read more about this in question 5: "When should sustainability annual reports be submitted?").

Step 6. External communication of the report

In addition to submitting your report to the authorities, companies are expected to make it publicly accessible. This can be done through annual reports or your company website. It is important that your stakeholders and investors have access to the report and that there is transparent communication about your company's sustainability efforts and results.

Although micro, small, and medium-sized enterprises (SMEs) that are not publicly traded are not obligated to comply with the CSRD, the regulations may still be relevant. Here are several reasons:

- Supply chain: Large companies that fall under the CSRD must report on the sustainability performance of their entire value chain, including their suppliers. This means that small and medium-sized enterprises (SMEs) that supply these companies may indirectly encounter the CSRD. Large companies may ask them for information about their sustainability policies so they can meet their own reporting obligations.

- Access to financing: Small and medium-sized organizations that implement sustainability may gain access to more favorable financing conditions, subsidies, or tax benefits.

- Future regulations: Although SMEs are not currently obligated, future regulations may emerge that apply to them as well. By voluntarily reporting or integrating sustainable practices now, your company can better prepare itself.

- Market advantages: Sustainability is increasingly becoming a requirement in many industries. SMEs that are proactive and integrate sustainability may become more attractive to customers, investors, and large companies looking for partners who adhere to sustainability standards. As a result, a sustainability strategy can provide SMEs with a competitive edge.

Examples can help provide insight into how other companies are approaching their reporting obligations under the CSRD. Below you will find where to look for several examples:

- Sustainability Disclosure Database van de Europese Commissie: Companies reporting under the CSRD will need to publish through this channel in the future.

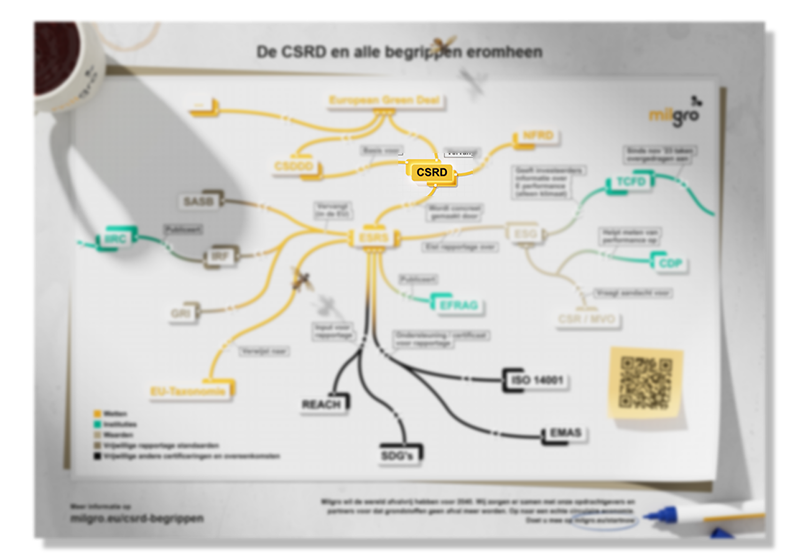

- Global Reporting Initiative (GRI) is one of the most widely used sustainability standards in the world. The website offers a database of sustainability reports from thousands of companies that comply with the GRI standards.

- Carbon Disclosusre Project (CDP) collects data from companies about their climate performance, water usage, and impact on deforestation.

- Corporate companies such as Unilever, Shell, and Philips publish their sustainability reports directly on their own websites under the sections "Sustainability" or "Corporate Responsibility." These reports can serve as good examples for your organization.

For more information on the CSRD guidelines, you can visit the European Commission's website. They provide free access to official documents and guidelines regarding the reporting obligation.

Above, we briefly discussed the Global Reporting Initiative (GRI), which provides a database of thousands of companies that comply with GRI standards. Here, you can also find sustainability reports from companies operating globally, giving you insight into how companies manage their ESG obligations (Environmental, Social, and Governance).

The RVO also provides information on the CSRD and how companies can comply with it. You can find this information here.

More about the CSRD

Looking for more information or support on integrating the CSRD directive? Download our free starter kit or roadmap so you can get started carefree. We also host regular webinars, efficiently navigating through the CSRD timeline so you can get started with practical tools right away.

Would you like to stay up to date with all the developments around CSRD? We regularly publish new blogs on the guideline. Follow us on LinkedIn or subscribe to our newsletter and stay informed.